What is a fund?

In essence, a fund is a pool of money set aside for a particular purpose. Typically, multiple investors will introduce money into a fund for a common purpose.

People create or participate in funds for diverse reasons. Our focus in this article is on those who are creating funds for the purpose of kick starting an entrepreneurial idea and giving it life. There are other contexts where a fund may be relevant that we will save for another day – for example, a family might set up an education fund for their children’s education. A couple might establish or participate in an established retirement fund so that they receive income on their retirement. We have written another article on those contexts, over here.

So how can funds be set up to be used to back a new idea / business?

Investment funds are pools of money set aside by people seeking a return on their investment. The investors’ funds provide equity that can be used by others and then redeemed according to the terms of the fund. The targeted return might be purely financial, or financial + societal or environmental or cultural. Increasingly such a broader conception of investment funds result in the term “Impact Investing” which we have written about separately here.

What structure might be used?

You might be able to get investors involved via debt – that is, they provide secured lending to you to undertake the project. Another option is via equity which is where investors have an ongoing ownership stake.

Typically a project that needs funding will be structured so that there is financial return for investors and this is often done with one of the following methods:

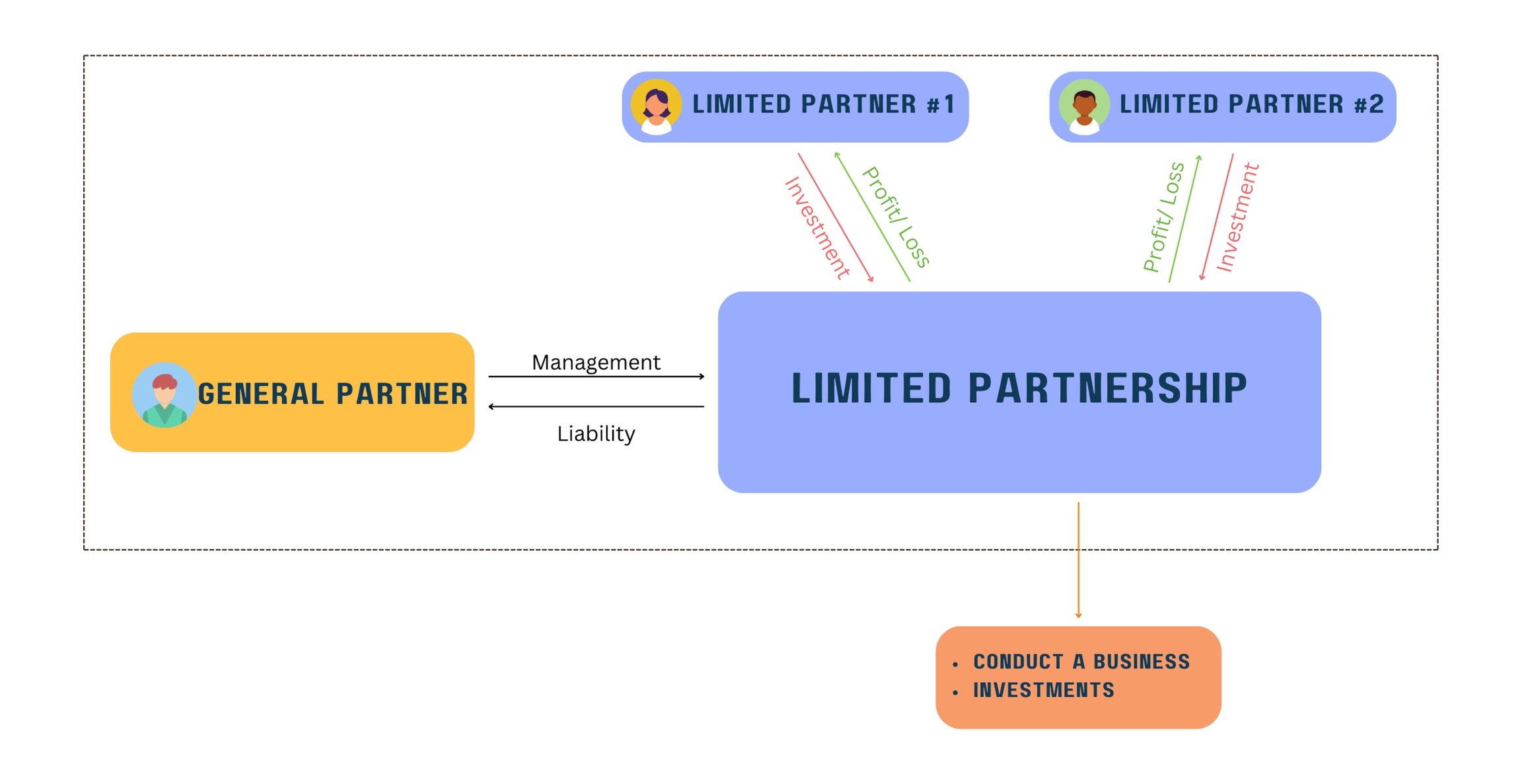

- Limited Partnerships – in this model for a fund there are those with money who invest but have little say in the project (limited partners) and there is an entity which guides the project (the general partner). This type of legal vehicle is useful when there is a distinct one off project, such as a housing development. There are often tax reasons why investors prefer this option as well. We go into more detail on this option here. An LP might also make loans to another entity which undertakes the project (so a combination of debt/equity structures).

- Companies – this is a traditional vehicle used to have investment and sees the money flow into the entity from shareholders who will then get return from the dividends that get issued when it is profitable. There will be directors of the company who make the key decisions for the project / business.

- Unincorporated Joint Ventures – another legal vehicle we see used from time to time is to have different parties involved in a joint venture which is set up for a specific project or purpose. While this is an option in terms of setting up a fund we would typically see that being overseen by an LP or company, mentioned earlier.

Other options may be worth considering, and we talk about different structures in this article here.

Ensuring you comply with fundraising rules

Whichever structure is chosen compliance with the rules set by the Financial Markets Conduct Act is critical – it sets out who you can solicit investment from. For example, if you only ask for investment from wealthy people (who are ‘wholesale investors’ as defined in the legislation) then you do not have as many compliance requirements in terms of the information provided to them. Depending on what the fund will do there may be other compliance which is needed, for example if financial services will be provided.

If you want to know more about this area, we suggest looking over our Capital Raising Guide here.

Please note that this is not a substitute for legal advice. We’d be delighted to discuss your situation with you, so feel free to contact us on 03 348 8480 or by email to Steven Moe – stevenmoe@parryfield.com or Kris Morrison – krismorrison@parryfield.com